Analysis of 3ABN's Form 990's from 1998 to 2006

With Emphasis on 2006

With no hint at all from Danny Shelton that he intends to back down from

his lawsuit over

Save3ABN.com, we venture to post this

analysis of 3ABN's financial situation, made possible by the availability of 3ABN's 2006 Form 990.

In this analysis we shall compare the facts with

Mollie Steenson's claim that "donations to

3ABN have decreased substantially since June 2006, when the Internet

commentary disparaging 3ABN and Danny Shelton erupted on various

sites on the Internet." This analysis may also shed some light on

why 3ABN is selling off some of its assets.

3ABN's Economic Difficulties Began in 2003, Not in 2006

Below is the cumulative data from 3ABN's Form 990's from 1998 through 2006. For each successive year, the

percentage change from the previous year is given.

| Year | Donations | ± % | Total Rev. | ± % | Total Exp. | ± % | Gain/Loss | ± % | Other Changes | Net Assets | ± % |

|---|

| 1998 | $7,557,624 | | $8,577,065 | | $6,759,968 | | $1,817,097 | | | $9,561,199 | |

| 1999 | $9,999,808 | +32.3% | $11,817,931 | +37.8% | $8,819,958 | +30.5% | $2,997,973 | +65.0% | ($46,158) | $12,513,013 | +30.1% |

| 2000 | $10,891,966 | +8.92% | $11,399,767 | −3.54% | $10,231,520 | +16.0% | $1,168,247 | −61.0% | $44,366 | $13,725,626 | +9.69% |

| 2001 | $12,323,162 | +13.1% | $13,450,381 | +18.0% | $11,469,091 | +12.1% | $1,981,290 | +69.6% | $2,450,614 | $18,157,530 | +32.3% |

| 2002 | $14,057,326 | +14.1% | $15,264,211 | +13.5% | $12,275,863 | +7.03% | $2,988,348 | +50.8% | $1,732,679 | $22,878,557 | +26.0% |

| 2003 | $10,902,656 | −22.4% | $11,481,779 | −24.8% | $13,561,929 | +10.5% | ($2,080,150) | −169.6% | | $20,798,407 | −9.09% |

| 2004 | $13,581,898 | +24.6% | $13,975,137 | +21.7% | $14,820,727 | +9.28% | ($845,590) | +59.4% | | $19,952,817 | −4.07% |

| 2005 | $14,060,275 | +3.52% | $14,956,597 | +7.02% | $15,439,090 | +4.17% | ($482,493) | +42.9% | | $19,470,324 | −2.42% |

| 2006 | $15,075,120 | +7.22% | $16,602,282 | +11.0% | $19,598,298 | +26.9% | ($2,996,016) | −621.0% | ($238,158) | $16,236,150 | −16.6% |

Based on the above data, several conclusions may be drawn:

- 3ABN's economic downturn began in 2003 when donations plummeted by more than 22%.

- 2003 was the year before Danny and Linda Shelton's divorce and several years before Save3ABN.com was launched. Thus, the beginning of the downturn is due to other causes than these.

- 3ABN has never fully recovered from the downturn in 2003, though donations finally did reach the levels of 2002 again in 2005, and then reached an all-time high in 2006.

- Expenses have continued to rise, and the all-time high for donations in 2006 was accompanied by a huge increase in expenses, resulting in a significant loss for that year.

- The cumulative loss from 2003 to 2006 was $6,404,249.

Why the Downturn in 2003?

Adventist Today suggested

that the sharp downturn in 2003 was due to the public becoming aware

of Danny Shelton's use of corporate jets rather than conventional commercial flights.

2003 was also the year that Roger Clem went public in the West Frankfort community with his allegations that

Tommy Shelton had molested him, and Pastor Glenn Dryden later wrote 3ABN Board chairman Walt

Thompson, informing him that the list of alleged victims was now six. Subsequently, Danny chose to

tell his 3ABN Board chairman that the allegations were 30 years old, Walt Thompson chose not to contact any

of the alleged victims, someone directed 3ABN Attorney Mike Riva to write a nasty cease and desist

letter to Pastor Dryden, and someone paid Mike Riva to do so, unless he did it pro bono.

At any rate, for whatever reasons, monetary blessings were not pouring out of the windows of heaven

as freely in 2003, resulting in a deficit of $2,080,150 that year.

Why the Strong Rebound in 2004?

The public was led to believe in 2004 that Linda Shelton had left her husband for another man. Understandably,

a lot of sympathy for Danny was created, and it is possible that this sympathy explains the stronger giving that

occurred in 2004. Yet, because expenses still continued to rise, there was still a $845,590

deficit that year.

The dramatic 2004 rebound did not continue into 2005, for donations increased by only 3.52% that year.

The smaller rise in expenses in 2005 kept the deficit down to just $482,493.

Implications for the Lawsuit

So are higher expenses and factors that began in 2003 the cause of 3ABN's economic woes, as the above data suggests,

or is the cause something that began in mid-2006, namely the various internet sites and

eventually Save3ABN.com that published concerns about

Danny Shelton's administration, as Danny's lawsuit

contends?

Recall also how 3ABN CFO Larry Ewing contradictorily claimed

in his affidavit

that the downturn simultaneously began in June, July, and October 2006, and that he supported that claim

by giving the percentage change in giving between 2005 and 2006 on a month by month basis. Yet he neglected

to give any real numbers, and understandably so. The real numbers indicate that 2006 was a banner year as

far as donation revenue was concerned.

But one claim that Danny Shelton has made that the numbers from

3ABN's 2006 Form 990 definitely do vindicate

is his December 6, 2006, contention that 2006

was 3ABN's "best year ever financially." Indeed it was, as far as revenue was concerned.

Another factor that is difficult to evaluate due to the Ten Commandments Twice Removed

campaign is Danny Shelton's remarriage in March 2006. To what

extent did his remarriage, apart from any publicity on the internet, affect donations, something that

couldn't be expected to be seen until the Ten Commandments Twice Removed massive fund-raising drive was over?

What Those Extra Expenses Were

So exactly why have expenses been so high, and have they all been necessary?

The Corporate Jets and Travel Expenses

In the table below, columns consisting of our calculated figures have headings that are contained in brackets.

Those calculated figures are based on the other figures in the table, which came from 3ABN's

Form 990's and financial statements.

The following figures suggest that travel expenses escalated after the Mitsubishi Diamond was purchased around 2001,

and the Cessna Citation was leased around 2003.

| Year | Travel on the 990

(Part II Line 39) | ± % | Travel on the Financial Statements |

|---|

Manage-

ment | Program Services | Total | Manag. Auto | Manag. Travel | [Total Manag.] | Prog. Serv. Airplane | Prog. Serv. Travel | [Total Prog. Serv.] | [Total Travel] |

|---|

| 1998 | $160,634 | | $160,634 | | | | | | | | |

| 1999 | $213,793 | | $213,793 | +33.1% | | | | | | | |

| 2000 | $282,402 | | $282,402 | +32.1% | | | | | | | |

| 2001 | $541,785 | | $541,785 | +91.9% | | | | | | | |

| 2002 | $595,982 | | $595,982 | +10.0% | | | | | | | |

| 2003 | $212,616 | $999,758 | $1,212,374 | +103% | $43,259.47 | $169,356.26 | $212,615.73 | $857,528.60 | $142,229.68 | $999,758.28 | $1,212,374.01 |

| 2004 | $255,423 | $1,144,093 | $1,399,516 | +15.4% | $80,554.84 | $174,867.92 | $255,422.76 | $989,438.91 | $154,654.42 | $1,144,093.33 | $1,399,516.09 |

| 2005 | $292,908 | $1,094,779 | $1,387,687 | −0.85% | $75,801.88 | $217,106.21 | $292,908.09 | $896,993.46 | $197,785.21 | $1,094,778.67 | $1,387,686.76 |

| 2006 | $284,761 | $1,208,788 | $1,493,549 | +7.63% | | | | | | | |

To oversimplify matters, of the $6,404,249 cumulative loss from 2003 to 2006,

the additional travel expenses attributable to the corporate jets amount to roughly $4,000,000 of that total.

We received word from one source that the 2003 figure of $857,528.60 for the jet does not include the half a million dollars that it cost to

repair or replace a blown engine.

Another point of interest might be how exactly the item labeled "Auto" was spent, since it is listed in the

financial statements as a separate item

from travel. Is this the category where the costs of the purchase, maintenance, and operation of the "company car for

business purposes" provided to Danny Shelton are to be found? (See Attorney Mike Riva's claim in

court documents.)

Book Sales ... That Weren't Sales ... After 2003

What follows below is data from 3ABN's Form 990's and financial statements concerning the accounting of

cost of goods when inventory items are sold or given away.

Books that were given away, including the Ten Commandments Twice Removed book, are presumably

part of the Cost of Goods Given Away category, but definitely not in 2003, for there was no such category that year,

and sales of books and such were lumped in with satellites in the Form 990.

Book Sales from the 990's

The "[Adjusted Gross Profit]" column consists of "Gross Profit" minus "Cost of Goods Given Away" minus "Inventory Write-Down."

"Cost of Goods Sold – Satellites" from the attachments is not included for

redundancy but to avoid confusion about the $2 discrepancy in 2002 between that figure and "Cost of Goods Sold."

The error is in the original.

| Year | 990 Sales of Inventory

(Part I Line 10) | 990 Attached Statements |

|---|

| Gross Sales | Cost of Goods Sold | Gross Profit | Cost of Goods Given Away | Inventory Write-Down | [Adjusted Gross Profit] | Cost of Goods Sold – Satellites |

|---|

| 1998 | $796,218 | $712,201 | $84,017 | | | | |

| 1999 | $3,895,025 | $2,908,224 | $986,801 | | | | |

| 2000 | $2,665,398 | $2,995,089 | ($329,691) | | | | |

| 2001 | $618,832 | $460,500 | $158,332 | | | | $460,500 |

| 2002 | $1,184,297 | $687,151 | $497,146 | | | | $687,153 |

| 2003 | $1,390,946 | $1,041,702 | $349,244 | | | | $1,041,702 |

| 2004 | $713,725 | $584,020 | $129,705 | $330,242 | | ($200,537) | $584,020 |

| 2005 | $864,361 | $609,669 | $254,692 | $605,744 | $278,700 | ($629,752) | $609,669 |

| 2006 | $1,164,615 | $1,001,811 | $162,804 | $3,167,235 | $72,369 | ($3,076,800) | $1,001,811 |

Notice the huge jump in "Cost of Goods Given Away" for 2006? 4.5 million copies of Ten Commandments

Twice Removed definitely cost quite a bit.

Financial Statements Document Accounting Change in 2003

Now for the data from the financial statements. This data shows that book, CD, and video sales were handled

like normal sales in 2003, but not in 2004 and 2005. For the latter two years they were treated as

if they were given away, thus suggesting that whatever was paid for those items was lumped in with donations

rather than reported as gross receipts for sales.

Such a change would have four effects:

- Donations would be padded with book, CD, and video sales, thus preventing anyone from knowing exactly what the real annual donations were.

- The public would also be prevented from knowing exactly how much the book, CD, and video sales amounted to, as well as what profits were realized from those sales.

- Thus, while donations in 2004 appear to rebound after the sharp decline in 2003, to what extent this was actually the case cannot be known because of this juggling of the numbers.

- It likewise cannot be ascertained what allegedly declined in 2006 due to criticisms on the internet. Was it book, CD, and video sales, or was it out and out donations, or both?

| Year | Data from the Financial Statements |

|---|

| Satellites | Other | Inventory Write- Down | [Totals] |

|---|

| Sales | Cost of Goods | [Profit] | Sales | Cost of Goods | [Profit] | [Sales] | [Cost of Goods & Write-Down] | [Profit] |

|---|

| 2003 | $991,604.39 | $887,536.04 | $104,068.35 | $399,341.21 | $154,165.62 | $245,175.59 | | $1,390,945.60 | $1,041,701.66 | $349,243.94 |

| 2004 | $713,725.32 | $584,019.94 | $129,705.38 | ??? | $330,242.46 | ($330,242.46) | | $713,725.32 | $914,262.40 | ($200,537.08) |

| 2005 | $864,361.26 | $609,669.09 | $254,692.17 | ??? | $605,744.30 | ($605,744.30) | $278,700 | $864,361.26 | $1,494,113.39 | ($629,752.13) |

In 2003, $245,175.59 profit on book, CD, and video sales was made on a $154,165.62 investment (cost of goods).

That's an extremely healthy 159% profit.

The 2004 Property Tax Case Decision

Another consequence of the change after 2004, intentional or otherwise, is quite

interesting in light of Judge Rowe's January 28, 2004, decision in

3 Angels Broadcasting Network

v. The Department of Revenue of the State of Illinois. 3ABN's attorneys have sought to drive

home the point that little or no profits are being made on sales. In 2003, over 70% of total profits from

all sales that year came from book, CD, and video sales. By changing the accounting system so that such sales are treated

as gifts, and receipts from such sales are treated as donations, perhaps 70% or more of profits from all sales

are thus hidden in the financial statements and Form 990's. This apparent lowering of profits in these

financial documents lends support to the legal arguments of 3ABN's attorneys.

As Attorney Mike Riva made clear in a court

document filed in 2005:

|

G. Pricing and Revenue of Religious Materials.

"Along with its TV broadcasts, Three Angels also distributes

its message via video and audio tapes, CDs, books, and other

types of literature that are all consistent with the Adventist

message. ... At times these items are given away, at

other times, a nominal fee is charged to cover a portion of the

costs of the item. ... If an item is

sold, the price is set based on affordability to the donors rather

than based on the need to cover the costs of the item. ...

There is no evidence that any items are sold at more than cost ....

"Revenue attributed to the sales of books, tapes,

videos, CDs, satellite dishes, or any other material Three Angels

sells did not exceed the expenses associated with purchasing,

promoting or distributing those items."

|

How 3ABN Attorney Mike Riva can make the claim in 2005 that "there

is no evidence that any [video and audio tapes, CDs, books, and other types of literature]

are sold at more than cost" in light of the fact that, according to 3ABN's 2003

financial statement, 3ABN made 159% profit on the sales of such materials, is unknown.

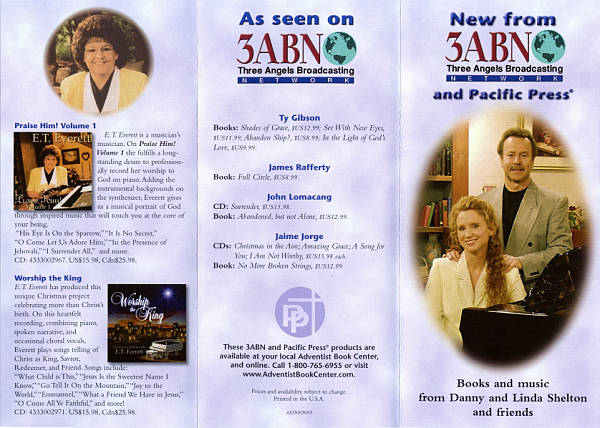

Are They Being Given Away or Being Sold?

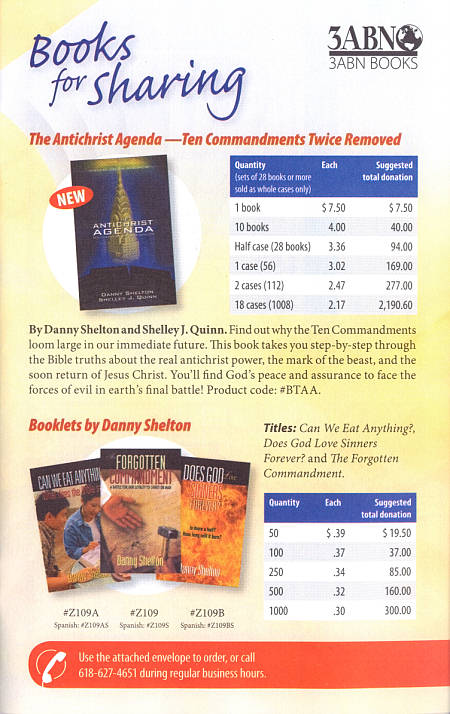

Below is a tri-fold flyer that was circulating in 2002. It presents more than 20 different products coming

from 3ABN and Pacific Press, each for a stated price.

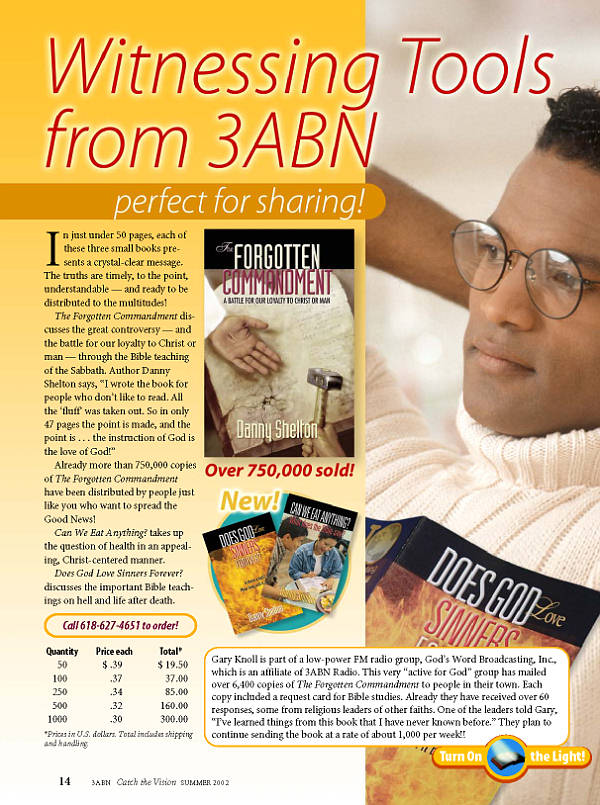

The following is page 14 from the summer 2002 issue of 3ABN's Catch the Vision,

advertising items for sale from 3ABN. By that point in time Danny Shelton's The Forgotten Commandment

had reached "Over 750,000 Sold!" rather than "Over 750,000 Given Away!"

The following was an insert in the 2005 issue of Catch the Vision. While prices are now called

"Suggested total donation," it still says "sets of 28 books or more sold as whole cases only." Thus,

products are still being sold rather than given away.

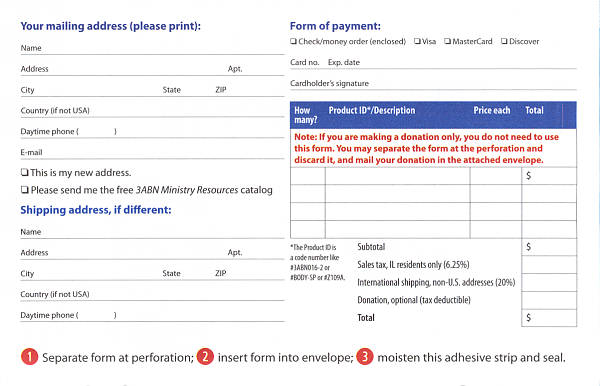

The following is another portion of the above insert, with a column to write in the "Price each" and

a place to put in "Sales tax" if you live in Illinois. If the only items now being sold are satellites and

everything else is being given away rather than being sold, as

3ABN's 2004 through 2006 Form 990's would have us believe, one would think that terms like "price" and

"sales tax" would not be applicable.

Taking the Numbers at Face Value Yields Different Conclusion

Now let's ignore all the above discussion for the moment and simply take the numbers of the 2004 through 2006

Form 990's at face value: A cumulative $4,103,221 worth of materials, everything but satellites,

was simply given away during those three years.

Taking these numbers at face value suggests that while Danny Shelton and others have been selling

books and such to 3ABN at a profit, 3ABN has not been doing likewise.

One might therefore conclude that if all along 3ABN had been purchasing materials at a normal retailer's

discount, and then selling those materials at a price a retailer would sell them at

in order to remain in business, perhaps a good bit of 2003 to 2006's cumulative loss of

$6,404,249 would never have occurred.

Someone definitely made a profit on the 2006 Ten Commandments Twice Removed campaign.

The information given in 3ABN's

2006 Form 990 can lead one to conclude that it just wasn't 3ABN.

Love Gifts

Another item that could be looked at is Love Gifts, which is sometimes lumped in with Miscellaneous on the Form 990.

There have been allegations that these love gifts have often gone to Shelton family members.

The careful reader will note that in 2003, "Love Gifts" plus "School Subsidy" plus

"Management Miscellaneous" from the financial statement amounted to about $5,272 more than

"Miscellaneous" on the Form 990. This is because "Repair and Maintenance — Equipment" on the

financial statement was that same amount less than "Equipment Rental and Maintenance"

on the 990. So either the audited financial statement

of April 14, 2004, or the Form 990 completed on June 24, 2004, is in error.

| Year | 990 Miscellaneous & Donations

(Attachments or Written In) | Figures from the Financial Statements |

|---|

| Prog. Serv. Misc. | Manag. Misc. | Total Misc. | Donations | Love Gifts | School Subsidy | Bad Debt | [Total] | [Manag. Misc. Added] |

|---|

| 1998 | N/A | N/A | N/A | | | | | | |

| 1999 | $23,603 | $30,515 | $54,118 | | | | | | |

| 2000 | $24,284 | $33,612 | $57,896 | | | | | | |

| 2001 | $100,737 | $106,265 | $207,002 | | | | | | |

| 2002 | $220,460 | $167,825 | $388,285 | | | | | | |

| 2003 | | $192,799 | $192,799 | | $109,754.87 | $54,741.49 | | $164,496.36 | $198,071.66 |

| 2004 | | $144,618 | $144,618 | | $54,132.36 | $70,541.29 | $1,710.54 | $124,673.65 | $144,617.74 |

| 2005 | | $35,783 | $35,783 | $216,636 | $133,673.50 | $82,962.06 | | $216,635.56 | $252,418.53 |

| 2006 | | $76,643 | $76,643 | $228,484 | | | | | |

So what exactly is "School Subsidy"? It is said to be a subsidy that goes toward the elementary

school on 3ABN's campus, at which children of Thompsonville Seventh-day Adventist Church members can

attend tuition free. It thus appears to be an extra benefit that 3ABN employees indirectly receive,

if they send their kids to that school and if they are members of that particular local church.

Line 89b on the 2006 Form 990

Unlike previous years, Line 89b on 3ABN's 2006 Form 990

got left blank. Consistently in previous years,

it had always been checked "No," even in 1998

when it should have been checked "Yes."

Why would it have been left blank? We admit, leaving it blank would have been far better than answering "No"

if "Yes" was in order.

Perhaps Danny Shelton's receiving of free advertising and promotion of the Ten Commandments

Twice Removed book from 3ABN, promotion that enabled the sale of 4.5 million copies and that allegedly resulted

in his earning several hundred thousand dollars of royalties, might constitute a section 4958 excess

benefit transaction.

|